There was a time when every budget cycle followed a familiar script. The National Treasury would propose new taxes, Parliament would amend them, businesses would complain, and the Kenya Revenue Authority (KRA) would be tasked with collecting more revenue than the year before.

That script was shattered in June 2024. The nationwide protests against the Finance Bill fundamentally altered Kenya’s fiscal politics. The withdrawal of the Bill did more than deny the government billions in projected revenue; it also forced a rethink of how the state would finance itself.

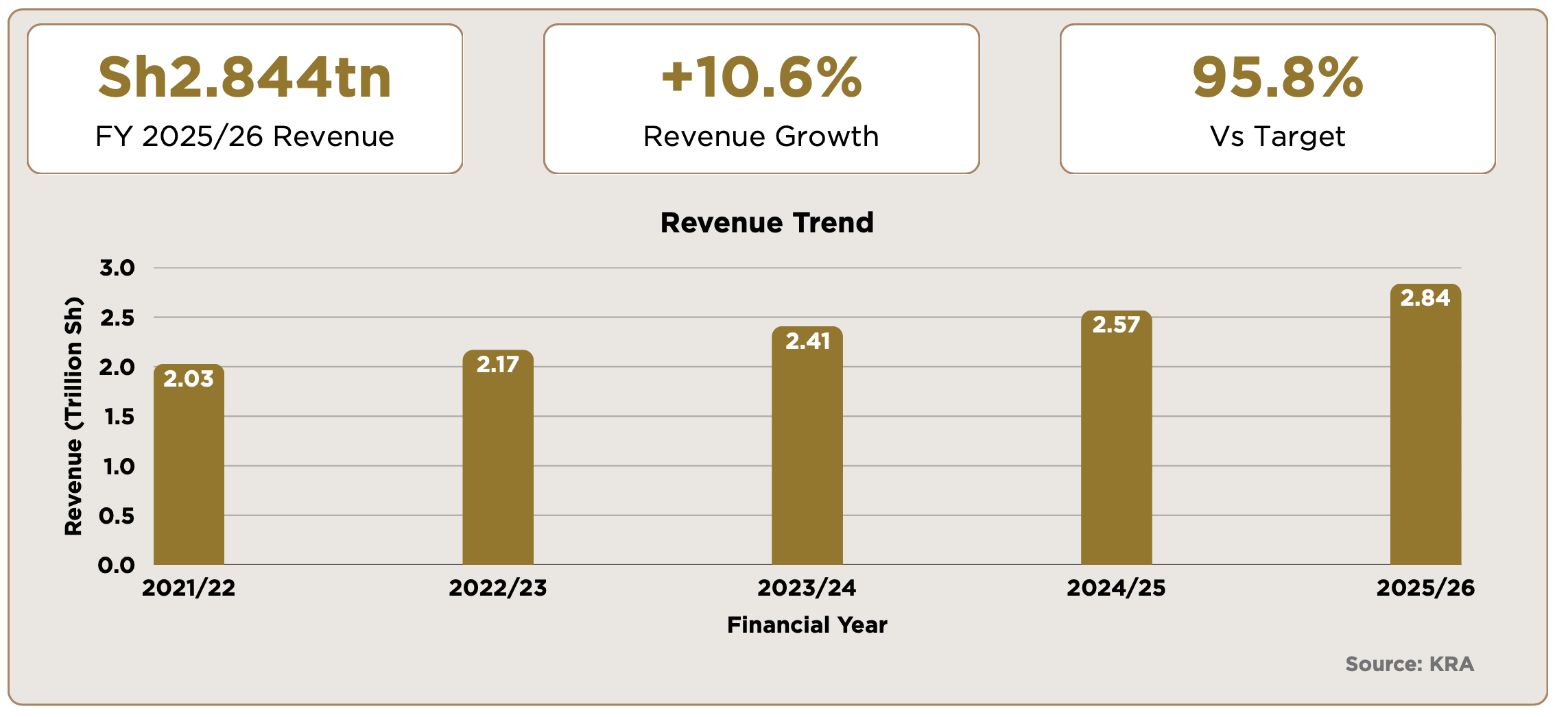

New taxes had become politically expensive. The path to higher revenue would have to come from somewhere else. The KRA’s performance for the 2025/26 financial year suggests it has found an answer. The authority collected Sh2.844 trillion, representing a 10.6 per cent increase over the previous financial year and one of the strongest annual growth rates in recent years.

The additional Sh273 billion collected in a single year is significant not only because of its size, but because it was achieved without a sweeping package of new tax measures comparable to those proposed in the controversial Finance Bill 2024.

The numbers point to an important shift in Kenya’s tax strategy. Rather than asking taxpayers to pay more through new levies, the government has concentrated on ensuring more taxpayers comply with the taxes that already exist.

From Tax Policy to Tax Administration

For years, Kenya’s fiscal debate centred on tax policy; what should be taxed, by how much, and who should pay. Increasingly, however, the conversation is shifting towards tax administration.

KRA has spent the past three years quietly investing in digital systems that allow it to identify undeclared income, match taxpayer information across multiple databases and reduce opportunities for tax evasion.

Electronic Tax Invoice Management System (eTIMS), expanded digital filing, improved customs monitoring, enhanced risk profiling, and data analytics have transformed how the authority approaches compliance.

These tools do not necessarily create new taxes, but they make existing taxes harder to avoid, and that distinction matters. Politically, improving compliance is easier to defend than introducing fresh tax burdens. Economically, it broadens the tax base without immediately increasing the cost of doing business for compliant taxpayers.

In many respects, KRA’s latest results demonstrate that enforcement has become the government’s preferred fiscal instrument.

The Economy Helped Too

It would be misleading, however, to attribute the entire performance to enforcement alone. The Kenyan economy has shown greater resilience over the past year than many analysts expected.

Inflation has moderated considerably, the exchange rate has stabilised after the volatility of 2023 and early 2024, agricultural production has improved following better rainfall, and sectors such as manufacturing, financial services, wholesale and retail trade, telecommunications and imports have continued to recover.

As economic activity expands, tax collections naturally rise. Corporate profits generate higher tax, increased consumer spending raises Value Added Tax (VAT) receipts, higher imports translate into stronger customs revenues, and growth in employment boosts Pay As You Earn (PAYE) collections.

KRA’s success, therefore, reflects both stronger administration and a gradually improving economy as the two reinforce each other. Digital enforcement is most effective when there is genuine economic activity to tax. The protests of 2024 changed more than fiscal policy as they also altered the relationship between government and taxpayers.

For perhaps the first time in Kenya’s recent history, public debate shifted from whether the government needed more money to whether citizens were receiving sufficient value for the taxes they already paid.

Questions about accountability, transparency and public expenditure became inseparable from conversations about taxation. That political reality has constrained the government’s room for manoeuvre.

It is no coincidence that recent fiscal strategy has emphasised compliance, efficiency and broadening the tax base rather than introducing headline- grabbing new taxes. KRA’s record collections suggest that the approach has worked, at least in the short term. But the strategy has limits.

Easy Gains May Be Behind Us

Every tax administration experiences diminishing returns. The first gains from digitisation are often dramatic because they capture taxpayers who were previously invisible or under-reporting their obligations. Over time, however, those gains become harder to replicate.

Most large formal businesses are already registered and monitored. Many medium-sized enterprises are now integrated into digital tax systems. The remaining untaxed segments of the economy are increasingly concentrated in informal businesses, cash-based transactions and sectors that are inherently difficult to regulate.

Extracting additional revenue from these areas will require considerably more effort and may provoke renewed resistance if enforcement is perceived as punitive.

The challenge is compounded by the structure of Kenya’s economy itself. Nearly four out of every five workers operate in the informal sector. While many informal businesses contribute indirectly through consumption taxes such as VAT, relatively few are captured fully within the income tax system.

Bringing this segment into the tax net has frustrated successive governments for decades. Technology can help, but it cannot entirely overcome the structural realities of informality.

KRA’s performance also needs to be viewed within the broader context of Kenya’s public finances. A record collection does not automatically translate into fiscal comfort.

Government expenditure continues to outpace revenue growth in several critical areas. Debt servicing remains one of the largest items in the national budget.

Counties require increased transfers, and major infrastructure commitments continue. Demands for expanded social protection, education and healthcare spending have not diminished.

Higher revenue certainly eases fiscal pressure, but it does not eliminate it. The government’s long-term fiscal sustainability will depend not only on collecting taxes more efficiently but also on controlling expenditure, managing public debt prudently and sustaining robust economic growth. Revenue administration is only one side of the fiscal equation.

The Next Phase

The significance of KRA’s 2025/26 performance lies less in the headline number than in what it reveals about Kenya’s evolving fiscal model. The State appears to have accepted that politically contentious tax hikes are becoming increasingly difficult to sustain.

Instead, it is betting that technology, compliance and administrative efficiency can generate much of the additional revenue it requires.

That is a sensible strategy for it rewards compliant taxpayers, improves fairness and reduces opportunities for evasion. But it cannot substitute indefinitely for economic expansion.

Ultimately, tax systems do not create wealth; they redistribute a portion of it. The stronger and more productive the economy becomes, the easier it is to raise revenue without increasing the burden on individual taxpayers.

KRA deserves recognition for demonstrating that better administration can produce substantial revenue gains without relying on controversial new taxes. Its record performance suggests the authority has matured into a far more sophisticated institution than it was a decade ago.

Yet the celebration should not obscure the bigger challenge. The next stage of Kenya’s fiscal journey will not be won simply by collecting more from existing taxpayers. It will depend on creating more businesses, more jobs, more investment and more productive economic activity to tax in the first place.

The lesson of 2025/26 is therefore not merely that Kenya has a smarter tax collector. It is that the country’s fiscal future will increasingly depend on whether the government can grow the economy faster than it grows its appetite for spending.