When President William Ruto stood next to American officials in Washington in May 2024 and announced a $1 billion data centre partnership with Microsoft and Abu Dhabi’s G42, the deal carried the polish of a turning-point moment.

The facility, planned for Olkaria in Naivasha, was meant to run on Kenyan geothermal energy, host Microsoft’s first East African Azure cloud region, and confirm Kenya’s status as the continent’s serious destination for AI infrastructure. The press conference framed it as the largest single private- sector digital investment in Kenya’s history.

The project has stalled after the Kenyan government failed to meet Microsoft’s demand for guaranteed annual capacity payments. And when Ruto eventually addressed the matter publicly, his explanation was stark enough to travel around the world.

“To switch on that one data centre, we would need to shut off power for half the country. That’s when I knew there was a problem,” Ruto said.

It is a sentence that says everything about the gap between Kenya’s digital ambitions and the physical infrastructure required to realise them.

The Numbers Behind the Admission

Kenya’s grid-connected installed capacity stands at 3,192 MW, with peak demand reaching a record 2,444 MW in January 2026. The Microsoft–G42 facility was designed to scale to a final capacity of 1 gigawatt (1,000 MW). Phase one alone was planned at 100 MW.

Even at phase one, the facility would have consumed roughly 4 per cent of national peak demand. At full build-out, it would have required more electricity than half the country uses at its busiest moment, approaching the combined peak consumption of Nairobi, Mombasa, Kisumu, and most of urban Kenya.

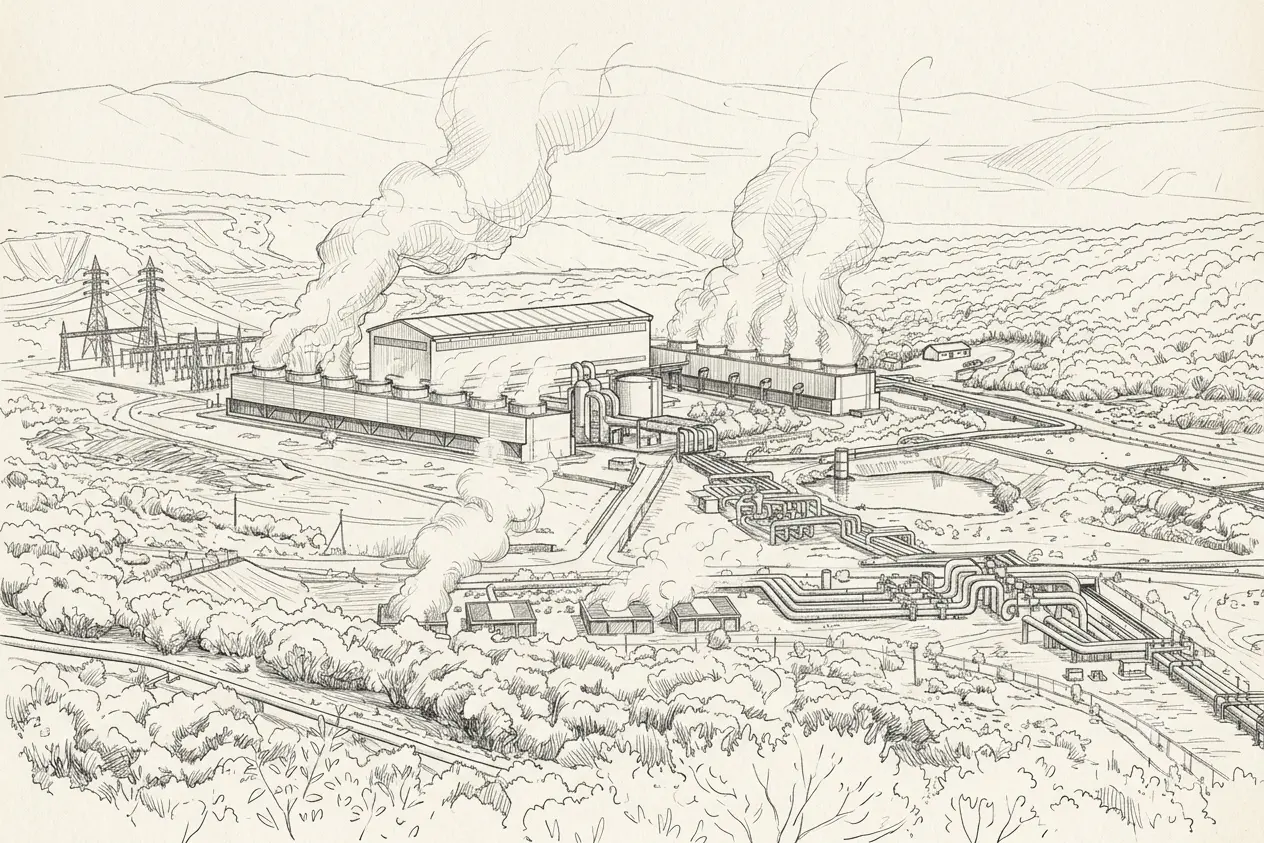

The Olkaria geothermal fields were the project’s core selling point. G42 CEO Peng Xiao said at the announcement that the full project would ultimately require as much as one gigawatt of electricity, and Olkaria, with its clean, 24-hour baseload power, was supposed to supply it.

The problem is that Olkaria’s geothermal complex generates roughly 950 MW today. Even tapping every single available megawatt would not be enough to supply the full data centre while continuing to serve the households and industries already drawing from that source.

The geothermal story has a second layer. Kenya lacks not just generation capacity but transmission capacity. A 100 MW data centre at Olkaria would need dedicated, high-capacity transmission lines before a single server could run, and that infrastructure gap is real and current

How a Flagship Deal Was Quietly Derailed

During a meeting between Kenyan government officials and Microsoft executives in August 2025, it became clear the data centre would not be online by its original target of May 2026. By that point, the project had already encountered a second, less-publicised obstacle.

A concept note prepared by Kenya’s Ministry of ICT was submitted to the National Treasury for funding clearance, and the approval never came. Negotiations faced complications over annual payment guarantees sought by the investors, and the government was unable to agree on the level of financial commitment requested to underwrite cloud demand.

Two blockers, then, not one: a grid that cannot supply the load, and a Treasury that would not guarantee the revenue. Together, they were enough to pause what had been presented as a done deal.

ICT Principal Secretary John Tanui has insisted that the project is “not failed or withdrawn,” noting that “the scale of the data centre they wanted to do still requires some structuring.”

That framing reflects a government trying to manage the reputational damage of a high-profile stall without conceding that the original announcement outran the available infrastructure by several years.

Lessons From South Africa

Microsoft has not pulled back from Africa. In April, the company announced a $329 million investment in South Africa focused on cloud and AI infrastructure, and critically, included upgrades to power and water readiness as part of the plan. South Africa has more grid capacity and, apparently, a more complete feasibility assessment.

The implication is uncomfortable: Microsoft evaluated both markets and found one of them investment- ready. It was not Kenya. Africa currently hosts roughly 1 per cent of the world’s data centre capacity, and the continent’s investor appetite for digital infrastructure is growing, but the foundational systems of power, water, and connectivity remain the bottleneck everywhere, Kenya included.

This is not a uniquely Kenyan problem. Nearly half of the planned US data centre builds in 2026 have been delayed or cancelled due to shortages of electrical infrastructure.

Microsoft is spending $190 billion on capital expenditure this year globally, adding approximately one gigawatt of data centre capacity every three months, but power constraints are proving a universal bottleneck.

What is uniquely Kenyan is that the power shortfall was apparently not identified and resolved before the presidential announcement was made. The ceremony came first. The feasibility study, it seems, came later.

What Kenya Actually Has, and What It Needs

The unfair reading of this story is that Kenya cannot handle big digital infrastructure. The accurate reading is more specific: Kenya cannot currently handle a data centre this large, on this timeline, without prior grid investment.

Kenya generates approximately 46 per cent of its electricity from geothermal sources, one of the highest ratios in the world, with Olkaria’s baseload steam operating at a 95 per cent availability rate.

The cost of geothermal energy in Kenya is approximately $0.07 per kilowatt-hour, significantly lower than the $0.18 per kilowatt-hour of thermal plants.

KenGen recently onboarded a fourth investor to its Green Energy Park in Olkaria: an industrial hub that allows companies to bypass traditional grid costs by setting up operations directly adjacent to the power source. That model may be the more realistic path for energy-intensive industries in the medium term.

Meanwhile, expansion is underway. KenGen received Cabinet approval for Olkaria VII, which will expand the complex’s installed capacity by 80.3 MW. Olkaria I is undergoing rehabilitation to increase its output from 45 MW to 61 MW by the end of 2026.

The Bigger Question

The Microsoft-G42 stall is not a technology or energy story. It is a governance story. It asks why a deal of this scale, one requiring grid infrastructure, transmission investment, Treasury guarantees, and a two-year construction programme, was announced at a presidential press conference before any of those foundations were in place.

Kenya’s situation feels less like an isolated problem and more like a preview of what the global AI race will start looking like everywhere: AI data centres are becoming so power-hungry that entire countries are beginning to rethink whether their grids can realistically support these projects without affecting ordinary citizens.

The difference is that most countries will reach that conclusion through quiet planning processes. Kenya reached it via a presidential admission at a state event, broadcast to the world.

The deal is not dead. Microsoft has not left. Kenya’s geothermal potential is estimated at 10,000 MW, a figure that, if developed, would make it one of the most attractive locations on the continent for energy-intensive industry.

But potential and readiness are different things, and the distance between them is measured not in megawatts but in years of grid investment, transmission upgrades, and Treasury planning that should have preceded, not followed, the announcement.

Kenya was chosen. The question now is whether it will be ready when it gets a second chance to be chosen again.