There is a moment, described more than once in a new report on Safaricom’s merchant payment product, Pochi la Biashara, that cuts through all the fintech strategy language and lands somewhere more human.

A woman trader in Kajiado County explains what changed when she started using Pochi la Biashara to separate her business earnings from her personal M-PESA wallet. Before, she says, she would see things and buy them unnecessarily. Her savings, she notes plainly, have increased.

That observation, and hundreds of others gathered across markets in Nairobi, Murang’a and Kajiado, sit at the centre of a report published in May 2026 by GSMA’s Mobile for Development programme, in collaboration with IDinsight and YUX.

Titled Pochi la Biashara and Women Micro-Entrepreneurs in Kenya, it documents a multi-year engagement between the GSMA’s Connected Women programme and Safaricom, and makes a quietly significant argument: that designing financial products around the specific pain points of women traders is not only good development policy. It is good business.

The baseline reality

Kenya’s informal economy is largely a women’s economy. Nearly three-quarters of working women in Kenya are self-employed, compared to just over half of working men.

Micro and small enterprises account for roughly fifteen million jobs and contribute the majority of non-farm employment in the country. Women run most of them.

Yet women micro-entrepreneurs have been consistently less likely than their male counterparts to use digital financial services for their businesses.

A 2022 GSMA consumer survey found that only 46 per cent of women micro-entrepreneurs surveyed had used mobile money for business in the previous three months, against 62 per cent of men.

The barriers are structural and familiar: lower digital literacy, safety and security concerns, restricted access to education and capital, and social norms that shape everything from how women interact with male customers to how they manage the competing demands of business and household.

These are not new findings. What the Pochi report contributes is evidence of what happens when a product is designed specifically to address those barriers, and what it takes to sustain adoption once it begins.

What Pochi solved

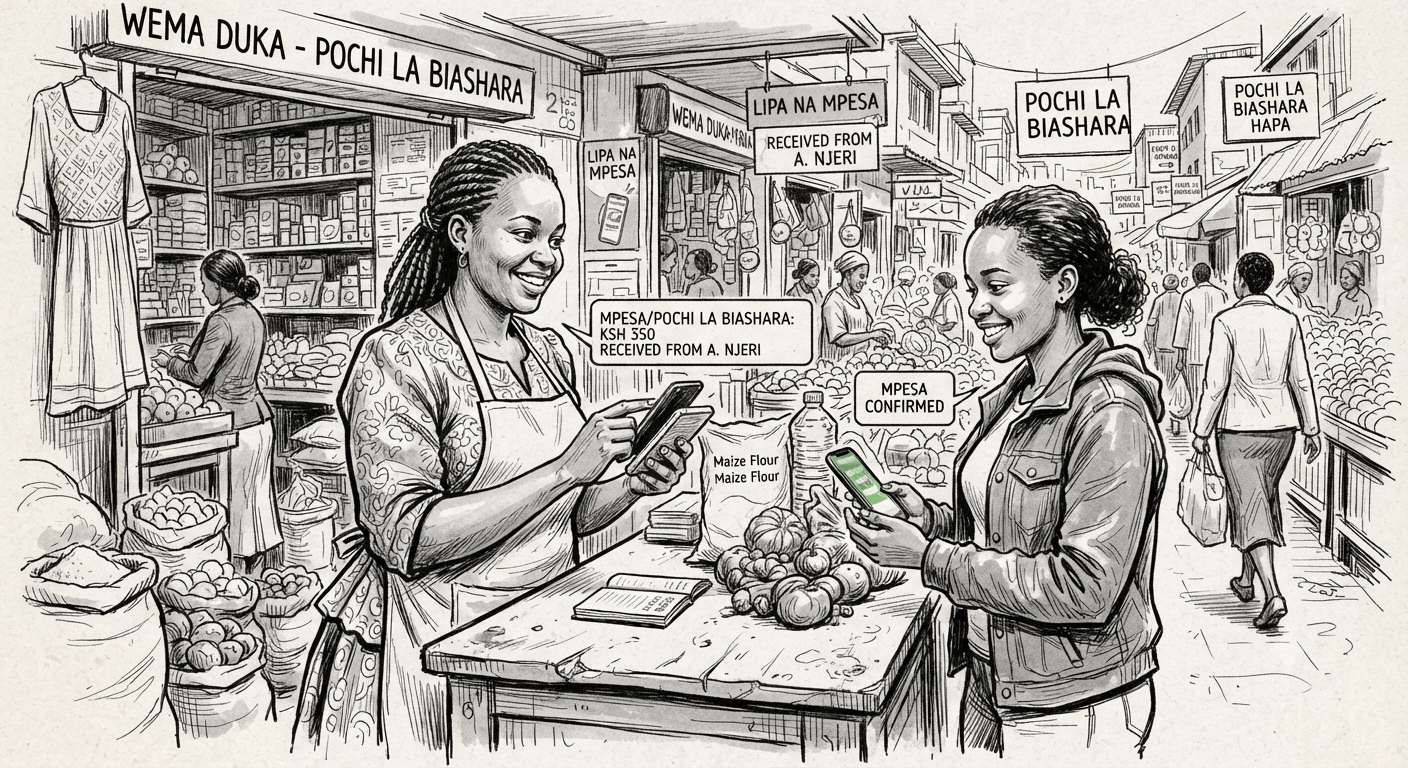

Launched by Safaricom in 2020, Pochi la Biashara is a merchant wallet linked to M-PESA that allows small traders to keep business earnings separate from personal funds.

The product was built around a clear diagnosis: women traders were losing money to payment reversals, struggling to track business finances when cash and personal funds mixed, and facing harassment when their phone numbers appeared publicly on payment stickers.

Pochi’s response was architectural. Non-reversibility of payments meant traders were protected from fraudulent chargebacks. The dual-wallet structure created a visible separation between business and personal money.

Mini-statements gave traders a daily transaction record. The product could be accessed via USSD, without a smartphone or data connection. These features were not incidental. They were, the report argues, the reason women adopted the product.

In the longitudinal study’s endline survey, 81 per cent of new users cited non-reversibility as their primary reason for preferring Pochi over alternatives like M-PESA Send Money or cash.

The mini-statement provided traders with something more intangible but equally significant: transparency over their own finances. As one trader in Murang’a County put it, she could now see what she sold, on which day, and how much was profit.

What adoption actually produced

The report’s impact data is self-reported and appropriately qualified; this is not a randomised controlled trial, but the direction of the findings is consistent.

Among women who adopted Pochi between the January 2025 baseline and the June 2025 endline, 35.6 per cent said they were now saving more money. Just under a quarter reported higher sales.

Around 11 per cent said their income had increased as a direct result of using the service. A smaller share reported reinvesting more in their business or purchasing higher volumes of stock.

What the data captures is a shift in financial agency, the sense that money which flows through a business is recognisably the business’s money, not a general pool subject to domestic pressure and opportunistic spending.

Several women described this in terms of control: over stock decisions, over savings discipline, over the ability to plan.

Safaricom’s business results track the same direction. Between December 2024 and December 2025, the number of women actively using Pochi grew by approximately 92 per cent, outpacing male user growth of 78 per cent.

By December 2025, women accounted for just over 52 per cent of all active Pochi users, more than 900,000 people, making it one of the few M- PESA products where women constitute the majority of the active base.

Revenue from Pochi reached Sh1.68 billion in the first half of the 2026 financial year, a year-on-year increase of 95 per cent.

The limits of awareness

The report is not triumphalist, and its most instructive findings may be the ones that complicate the adoption story. Awareness of Pochi features among users did not reliably translate into use of those features.

In the endline survey, 48 per cent of new users knew about the mini-statement function; only 8 per cent had used it. Seventy-one per cent were aware of Lipa na Pochi, the highest awareness of any feature, but 18 per cent of those users had never tried it. For the airtime resale function, awareness was at 34 per cent and actual usage at 7 per cent.

This gap is not a communications failure, exactly. It is a reminder that adoption is not a single event but a process; one that requires sustained engagement, demonstration and trust-building well beyond the moment of registration.

The Safaricom TDR network, the company’s field agents who move through informal markets and conduct live product demonstrations, was cited by 60 per cent of new users as the decisive factor in their decision to adopt Pochi.

Peer recommendation, typically from another businesswoman, was cited by 21 per cent. The implication for fintech design is direct: the channel through which women learn about a product matters as much as the product itself.

What the model suggests

Kenya is not a template. The conditions that made Pochi viable, an extensive M-PESA infrastructure, an established agent network, and high mobile penetration, do not exist by default elsewhere.

Text message campaigns and marketing collateral reached relatively few new users. Human interaction, grounded in demonstration and trust, drove the majority of uptake.

But the underlying logic of the product’s success is transferable: identify the specific economic risks and social vulnerabilities that make women reluctant to adopt digital financial tools, and build features that address them directly rather than treating those concerns as secondary.

For Kenyan women traders, that meant non- reversibility, number masking and USSD access. In other contexts, the design response would look different.

The principle that women’s economic participation expands when financial tools are built around how women actually live and work, rather than adapted from products built for someone else, is not context- specific at all.

The trader in Kajiado who now knows exactly what belongs to her shop already understood this.

The fintech industry is still catching up.