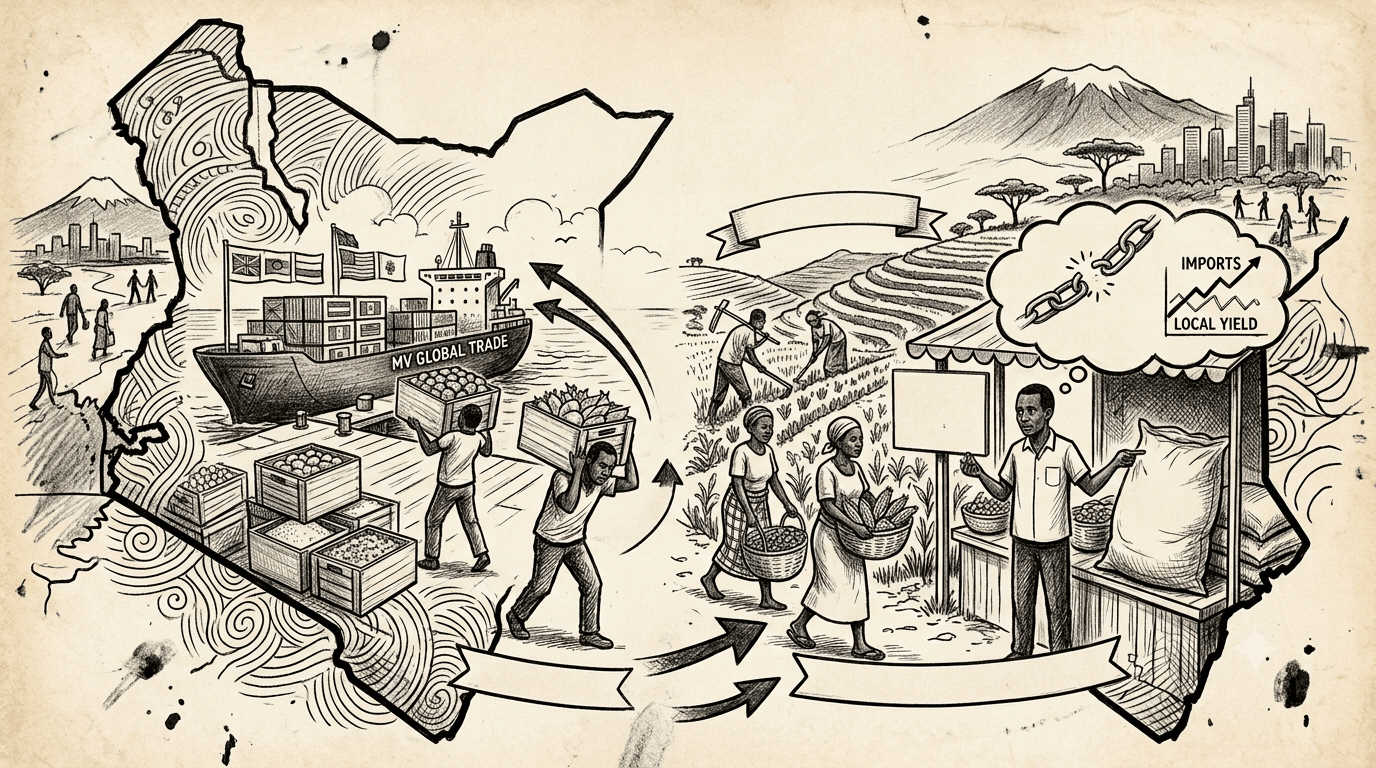

Kenya spends Sh160 billion annually importing edible oil. It currently produces just 306,000 tonnes of its 900,000-tonne need, importing the remaining, predominantly palm oil from Southeast Asia.

This is not a natural condition. Kenya has arable land, adequate rainfall across most agricultural zones, and a smallholder farming population with both the capacity and the incentive to grow sunflower, canola, soybean, and coconut at scale.

The edible oil import bill is the largest and most visible case of a pattern that runs across at least five other major commodities.

In each case, the story is structurally similar: a domestic production deficit that is closeable, a persistent import dependency that benefits a specific set of interests, and a reform agenda that has addressed the supply side without confronting the political economy of the distribution side.

Maize: A Claimed Victory Worth Scrutinising

Maize is Kenya’s most politically charged agricultural commodity. It provides over 40 per cent of daily calorie intake, anchors the food security debate, and has historically been the single most manipulated crop in the country’s agricultural system.

This has manifested in import exemptions and NCPB purchasing decisions, providing reliable channels for rent extraction by well-connected traders.

The current government’s claim on maize is its strongest agricultural headline: domestic imports reportedly fell from 10 million bags in 2022 to zero in 2025, attributed to the fertiliser subsidy programme and value chain support.

The US Department of Agriculture’s own 2026 forecast broadly supports the direction, projecting a 32 per cent surge in maize production to 4.5 million metric tonnes, potentially achieving near- equilibrium with consumption for the first time in years.

But the USDA is also explicit that Kenya will remain a net importer of maize in the 2025/26 marketing year, even with the production surge, due to ongoing local supply deficits.

The government’s “zero imports” claim and the USDA’s “still a net importer” projection are not easily reconciled, and the difference matters because a genuine break in maize import dependency would represent the first time in a generation that one of the most lucrative import channels in Kenya’s agricultural political economy has been closed.

Rice: 20% Domestic, 80% Imported

Kenya consumes approximately 1.3 million tonnes of rice annually. Local production contributes just 264,000 tonnes, covering 20 per cent of demand, with rice demand growing at over 10 per cent annually as urbanisation accelerates and dietary patterns shift toward wheat and rice-based foods.

To close the gap, the government has set a target of rice self-sufficiency by 2032, anchored on completing large-scale irrigation projects, including the Galana Kulalu Food Security Project, with Mwea, Ahero, and Bura irrigation schemes also earmarked for expansion in partnership with Japan.

The self-sufficiency target is technically achievable; nearly 80 per cent of Kenya’s domestic rice is already produced under irrigated ecologies, meaning the constraint is irrigation infrastructure rather than rainfall or soil suitability.

The State Department of Irrigation requires Sh50.75 billion for the 2025/26 financial year, but has only been allocated a fraction of that figure.

The gap between what irrigation expansion costs and what Treasury is willing to release is the single most honest explanation for why Kenya keeps approving duty-free rice imports as an emergency measure rather than building the infrastructure that would make them unnecessary.

Wheat: Russia’s Bread on Kenya’s Tables

Kenya consumes roughly 2.73 million metric tonnes of wheat annually, a figure growing at nearly 9 per cent per year as urban populations shift toward bread, pastries, and baked goods. Domestic production covers a small fraction of that demand.

Russia remains the largest exporter of wheat to Kenya, meaning the country’s most basic bread staple is priced in dollars, shipped across two oceans, and subject to geopolitical supply shocks, as the Middle East conflict-related disruptions in 2026 have illustrated directly.

The Wheat Purchase Programme nominally obligates registered millers to buy all locally produced wheat before accessing import licences.

In practice, millers have significant discretion in how energetically they pursue local sourcing, and the incentive structure has historically rewarded importing over investing in domestic supply chains.

USDA projects a 5.6 per cent decline in wheat production for 2025/26, as farmers shift away to alternative crops like barley and canola, due to complications in the domestic support programme. Import dependency in wheat is, on current trends, deepening rather than closing.

Edible Oil: The Biggest Bill, the Longest Road

The Edible Oil Crops Promotion Project, launched in July 2023 at Sh981 million, aims to raise domestic production from 80,000 to 240,000 metric tonnes over five years, nearly tripling current output, though still well short of the 900,000-tonne national need.

Current productivity in oil crop farming averages just 0.3 to 0.5 tonnes per hectare; improved inputs and agronomic support are expected to raise yields to around 2 tonnes per hectare. These are achievable numbers.

The programme has so far distributed canola seeds across 11 sub-counties in Nakuru, covering 1,250 acres, a meaningful pilot, and a fraction of the 250,000-hectare cultivation target.

The more important question is not whether domestic oil crop production can improve. It clearly can.

The question is whether the licensing, distribution, and procurement systems that make cheap Southeast Asian palm oil consistently more attractive than domestically grown sunflower oil will be restructured. So far, that conversation has not happened in public.

The government claims Kenya has effectively broken a 22-year sugar import cycle, with domestic production exceeding 900,000 metric tonnes against consumption of approximately one million tonnes, a remarkable claim if accurate.

Independent analysis from the Institute of Economic Affairs found that Ruto’s assertion of an 80 per cent decline in sugar import costs was inconsistent with Kenya National Bureau of Statistics data showing import unit prices rose approximately 20 per cent between 2022 and 2023.

The 2026/27 budget allocates funds to waive historical debts crippling state-owned millers, a structural fix that has been partially funded in successive budget cycles since the 1990s without being fully resolved.

The Common Thread

What links edible oil, maize, rice, wheat, and sugar is not a shortage of agricultural potential. It is a shortage of political will to dismantle the specific interests that make import dependency profitable.

Those interests take different forms across different crops; the palm oil importer, the wheat miller, the maize trader with an NCPB relationship, the sugar smuggler, but they share a structural feature.

They are better organised, better resourced, and better connected than the smallholder farmers whose livelihoods depend on domestic production, finally competing on fair terms.

Kenya’s current agricultural reform agenda is the most serious attempt in a generation to shift the production equation.

Fertiliser subsidies, coffee liberalisation, oil crop promotion, irrigation investment, these are real interventions with real effects. What they have not yet done is name the import lobby, map its interests, and legislate against them.

Until that happens, Kenya will continue to spend Sh160 billion importing what its own farmers can grow, and reforming agriculture at the margins while leaving its political economy intact.